Healthcare organizations face unparalleled pressure to increase operating margins as they adapt to the revenue compression from COVID-19 and growing competition from insurers and digital disrupters. Yet, many health systems rely on outdated, revenue-centric cost accounting solutions that are ill equipped for strategic financial decision making. As a methodology for today’s complex healthcare environment, activity-based costing (ABC) can capture healthcare resource use at a granular level. With this service-level insight into clinical cost, ABC provides actionable intelligence to help organizations improve profitability and make strategic cost-reduction decisions. These comprehensive costing solutions give health systems a full understanding of cost across the care continuum—the only level of insight that will enable strategic cost transformation in the industry’s new normal.

As healthcare organizations adapt to the revenue compression from COVID-19 and increased competition from insurers and digital disrupters, strategic cost transformation is critical to success. To improve profitability and make strategic cost-reduction decisions, health systems need to fully understand and have line-of-sight visibility into their clinical costs. Estimates of costs and allocations of large pools of overhead are inaccurate and obsolete methods that cause financial teams to quickly lose credibility with physicians and administrators. Healthcare activity-based costing (ABC) is the only way to accurately measure and assess 100 percent of an organization’s clinical costs and understand who is consuming resources—where in the organization and for what purposes.

COVID-19 has elevated the need to prioritize cost. The pandemic’s impact on healthcare delivery models (e.g., the shift to virtual care and reduction in emergency department volumes) demands a new cost footprint that is sustainable and correctly matched with the related revenues. As many systems have yet to recover their traditional volume/revenue levels, the question remains whether some activity will ever return.

Also complicating healthcare’s financial future is the emergence of large insurers. These entities are making investments on the provider side, acquiring physicians and surgery centers or partnering with value-based primary care providers (e.g., Oak Street Health and ChenMed) to reduce utilization by Medicare patients. These initiatives aim to decrease the traditional fee-for-service volume that has driven provider growth and expansion over the years.

Current cost accounting solutions are likely ill equipped for this increasing complexity, as they are often revenue-focused and deliver generic or inaccurate costing models. Many are home-grown systems, difficult to maintain and rarely used in strategic decision making. Estimates and allocations are inherent in these methodologies, and they don’t capture healthcare resource use at a granular level or provide actionable intelligence.

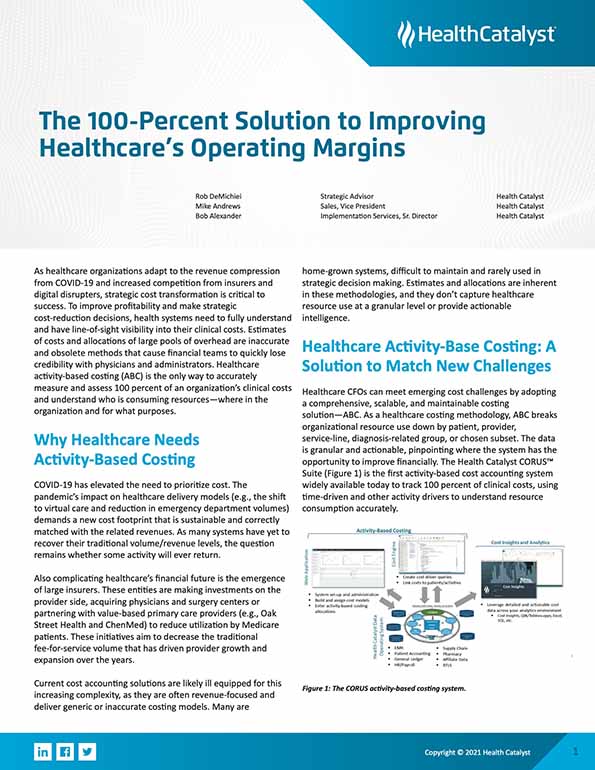

Healthcare CFOs can meet emerging cost challenges by adopting a comprehensive, scalable, and maintainable costing solution—ABC. As a healthcare costing methodology, ABC breaks organizational resource use down by patient, provider, service-line, diagnosis-related group, or chosen subset. The data is granular and actionable, pinpointing where the system has the opportunity to improve financially. The Health Catalyst PowerCosting™ is the first activity-based cost accounting system widely available today to track 100 percent of clinical costs, using time-driven and other activity drivers to understand resource consumption accurately.

The old methods of assigning cost reduction targets or setting across-the-board percentages for reduction will no longer work. Instead, ABC insights allow for new methods and approaches to optimize resource consumption and reduce costs.

The ABC methodology and insights of cost at a patient/physician level allow for rapid deployment and implementation of service-line management and provide insight into clinical practice variation and its impact on resource consumption and a framework for true cost productivity. Together, these capabilities allow for ongoing measurement and accountability around patient volumes and effective labor and resource optimization to ensure patient safety and operating efficiency.

Service-line management stands to grow as an essential capability. When hospitals affiliate with larger organizations, partnering entities often have inpatient and outpatient facilities that are geographically close to one another. This proximity provides both an opportunity and an imperative to optimize care delivery, quality, and cost efficiency in the service area—a service-line approach.

While health systems previously managed cost and clinical services within the four walls of the hospital or outpatient center, facilities’ geographic concentration likely creates overlap and the opportunity to look more holistically at the facility footprint, service offerings, and patient population/demographics. Clinical services may benefit in quality outcomes, patient safety, and cost productivity by consolidating offerings at fewer locations and creating specialty hospitals or branded/focused care locations instead of a general hospital with a full range of specialties.

While consolidating facilities and services may seem intuitive, organizations need crisp and comprehensive data, both clinically from the EMR and financially from decision-support systems. Aggregated data enables a full understanding of the activity levels, resources used, and ultimately the profitability. The general ledger most likely only records information by the location, and old costing solutions and methods don’t have the capability to create these service-line financials.

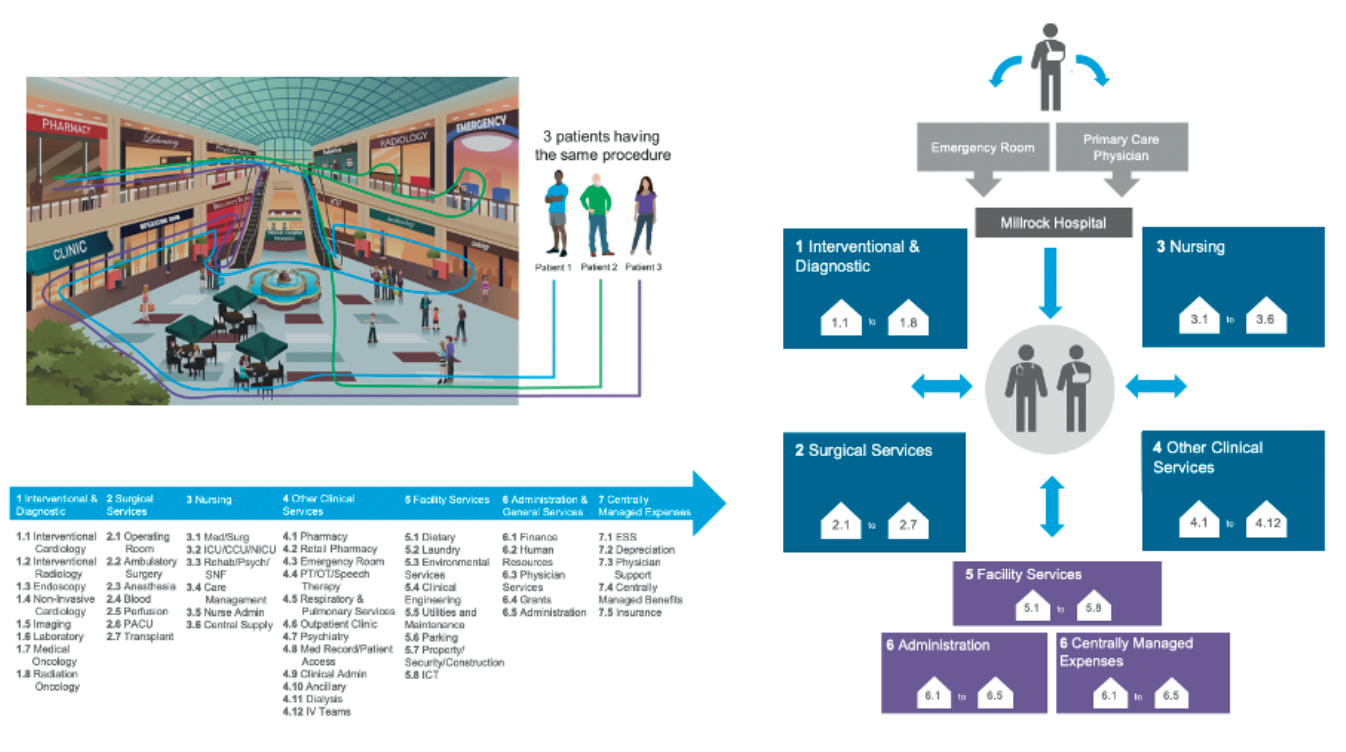

When organizations understand their costs at the service-line level, they can manage and optimize them. Service line management groups patients or populations by specific attributes (e.g., diagnosis, disease category, etc.). Healthcare service lines tend to be patient facing, with examples including orthopedics, oncology, pediatrics, neurosurgery, behavioral health, and more. Organizations can consider service lines equivalent to a traditional profit and loss (P&L) center, with full revenue and expense elements.

Service centers are integral to service line management because they provide critical services to the service lines. Examples include imaging, labs, nursing/ICU, and surgical services. Service centers may have a separate revenue stream but are more appropriately classified as cost centers rather than service lines. They primarily support all areas, physicians, and service lines, providing critical services and support to the patient.

Service lines and centers work together in the diagnosis and treatment of patients. They frequently interact during the patient’s care journey; service-line physicians’ clinical decision-making and practice patterns often drive consumption of service-center resources. However, separate physician and administrative executives often lead service lines and centers, and organizations financially track and measure them separately.

Given the service-line/service-center relationship, an accurate costing methodology must track and account for resource consumption throughout the care journey. Cost-accounting solutions need the ability to record all specific costs incurred, no matter the department or area of the hospital. The ABC system can match the physician’s decision-making throughout the care journey to the actual consumption of resources and cost (full-consumption costing), fully leveraging a wealth of clinical information in the EMR (Figure 1). Clinical revenue is specifically matched to the inpatient episode or outpatient procedure, enabling accurate, timely, and systemic creation of service line P&L and profitability insights by patient/physician/procedure.

Generally, less than 50 percent of an organization’s total clinical costs are direct costs (e.g., medical-surgical supplies or pharmacy). The service centers generate the other 50 percent of the total cost (e.g., utilization of surgical services, labs, imaging, and the inpatient stay). As such, a cost-accounting solution must track 100 percent of clinical costs to control resource utilization, understand clinical variation, and identify opportunities to improve productivity. Tracking must include both the direct service-line costs and the indirect costs from the service centers. There is nothing “free” in healthcare. Care decisions result in the consumption of resources, and organizations must attribute the cost of consumption to the physician, procedure, and service line responsible for the decision.

Many of the home-grown cost accounting and productivity measurements, as well as the current software-as-a-service (SaaS) products in the market, only address the direct costs, making proprietary methods “50-percent solutions.” The incomplete solutions then use estimates or imprecise or incorrect allocation methodologies, such as relative value units (RVUs) or outdated standard costs, to allocate the service center costs. This can be a huge dissatisfier for clinicians, who often don’t recognize their practice patterns in these allocated costs; credibility and physician support for cost accounting can quickly fade.

As a result of incomplete costing solutions, organizations often don’t accurately attribute resource consumption or clinical variation in the service centers to the corresponding service-line physician. Instead, organizations tend to hold hospital leadership solely accountable for over-budget outcomes instead of also holding accountable the physician placing the orders and making the care decisions.

Current cost-accounting solutions don’t properly match resource consumption to the physician’s decision-making nor highlight the significant variation between physicians in the same service line. For example, with an inpatient stay, who is responsible for length of stay (LOS)? Is it the hospital president or the unit director? Or is it the physician who ultimately makes the clinical decisions around surgical intervention, drug therapies, and discharge?

Length of stay is often “free” to the service line physician, meaning there is no tracking nor consequence for having a three- versus a four-day LOS, even though the more extended stay is more costly. Still, health systems often hold the hospital or nursing leadership accountable for over-budget LOS, not physicians. If an organization can’t properly measure the cost of the physician’s decision-making, how can it hold them accountable for delivering on healthcare’s Triple Aim?

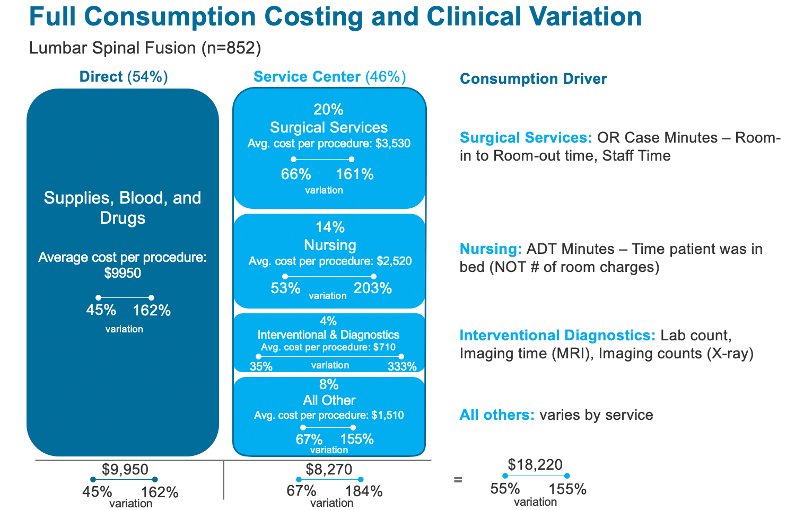

In the following example of one health system’s clinical variation in a lumbar spinal fusion procedure (Figure 2), throughout 852 procedures, service center costs were nearly half (46 percent) of the total cost. Although the average cost of the procedure was $18,220, the cost variation ranged from a low of 55 percent of the average to over 155 percent of the average—a clear opportunity for the health system to reduce variation.

The example above illustrates the significance of service center costs in the total cost of care and the significant variation in clinical practice and the resulting cost variation. ABC is the only solution that can accurately account for the entire cost of care and illustrate the significant transformation opportunity in reducing unnecessary clinical variation and the utilization of service center resources.

Clinicians and administrators need real-time data and self-serve capabilities around operating performance. They need the freedom to pose and answer questions about clinical efficiency, profitability (by procedure, clinician, and site), practice variation, resource optimization, and quality cost. As a solution, PowerCosting links seamlessly to an organization’s chosen visualization tools (e.g., QlikView®, Tableau, Power BI, etc.) with both pre-populated and ad hoc capability to deliver business intelligence.

With the data from clinical information systems linked to the financial systems at a patient-level, organizations can now use accurate data to find opportunities and solve previously unseen or unknown problems. Financial teams can identify real cost-reduction opportunities, reducing or eliminating the need for “across-the-board” cost reduction targets. Service-line leaders can look “horizontally” across the health system for potential redundancy and opportunities to consolidate and optimize care delivery and resources.

Many health systems have established resources and reporting to measure various aspects of operations, purporting to measure efficiency and assist the clinical areas in their business decision making. Many organizations publish numerous monthly statistical and budgetary reports. However, are the reports actionable? Are they a source of insight for physicians and operators? Does the system hold leaders accountable for productivity when volume varies or just for meeting the budget? Is an organization still measuring labor productivity using nursing hours as a proxy for cost?

In response to the above questions, an ABC solution, such as PowerCosting, provides simple but powerful productivity measures, utilizing the actual costs incurred in delivering the clinical care as the “input” measure and a suite of “output” volume measures to optimize. This capability ensures that an organization has a framework for cost productivity, starting at a global/system level, then drilling down to individual hospitals/outpatient facilities, and ultimately individual departments and units and service lines and service centers.

The following categories provide a framework for systemwide accountability and measurement, but the PowerCosting provides the capability to customize and add additional or alternative measurements. All measures are rooted in the idea of “cost per”; every clinical output is anchored to its resource (cost) input, providing a clear and comprehensive indication of the optimization of resources.

Clinical productivity and analytics comprise “cost per” metrics for all large cost, including the following:

In addition to the individual physician and service line P&L capability mentioned previously, ABC and the PowerCosting allow finance teams to automate the completion and reporting of monthly results and financial analysis. Instead of using multiple databases and clinical systems to retrieve operating data, the PowerCosting provides one source of truth by leveraging all available data from the EMR and other clinical systems.

Combine this data with financial information directly from the general ledger, and analysts now have a powerful workspace to analyze business results and fully automate report creation and preparation. This all-in-one financial planning and analysis concept fully leverages existing data to combine clinical and financial data to explain business results and trends. The concept also fully automates report creation and integrates seamlessly with available visualization tools, allowing teams to analyze the results and spend time with clinicians and administrators to democratize the information and improve operating performance.

Organizations must understand their costs comprehensively and accurately in an era marked by pandemic pressures and new entities and trends reshaping the healthcare financial landscape. As a comprehensive, transparent costing methodology, ABC solutions can help health systems transition from estimation-based cost accounting with limited visibility into the cost drivers to a full understanding of cost across the care continuum. This insight will enable the strategic cost transformation organizations must deliver in healthcare’s new normal.

Would you like to learn more about this topic? Here are some articles we suggest:

Would you like to use or share these concepts? Download the presentation highlighting the key main points.

https://www.slideshare.net/healthcatalyst1/the-100percent-solution-to-improving-healthcares-operating-margins